- LATEST

- WEBSTORY

- TRENDING

PERSONAL FINANCE

Stagger investments in Equity Linked Savings Scheme till end-March

It will help you get advantage of cost averaging to some extent, while meeting the tax-saving requirement through the equity route

Updated : Jan 16, 2019, 06:55 AM IST

"Equity Linked Savings Scheme")

TRENDING NOW

)

Aamir's biggest hit film's name changed thrice, was rejected by SRK, Salman, Saif, earned 3 times its budget, name was..

)

India's most profitable film, earned 6000% profit, one superstar cameo made movie blockbuster, actress left Bollywood

)

Meet Shah Rukh Khan's favourite actress who he had crush on; not Priyanka, Anushka, Deepika, Kajol, Rani, Juhi

)

India's most expensive film had 3 superstars, 2 crew members died, producer was arrested, still became highest-grosser

)

10 times XXX show actress Aabha Paul set Instagram on fire with sultry photos, sexy videos

)

Vikram on 'incomplete love story' with Aishwarya Rai amid her divorce rumours with Abhishek Bachchan: 'She's somebody..'

)

Amid affair rumours with Abhishek Bachchan, Nimrat Kaur talks about wedding plans: 'When you meet...'

)

Shah Rukh Khan gifts luxurious car to son AbRam, it is equipped with refrigerator, TV and costs Rs...

)

Bigg Boss 18: Netizens call Avinash Mishra 'the worst contestant in show's history' after he asks Chahat Pandey to...

)

Meet man who began his career with Tata Motors, now runs Rs 2690 crore company, married to...

)

Meet actress who was accidentally hit by a stuntman, refused films with Salman Khan, loves collecting...

)

Nirmat Kaur calls Abhishek Bachchan 'bloody lucky' after he makes this confession about Aishwarya Rai in viral video

)

Fabulous Lives Vs Bollywood Wives fame Shalini Passi's old photo with Gauri Khan goes viral, her husband was SRK's..

)

32-year-old superstar forcibly kissed 15-year-old co-star; left her traumatised, crying; later laughed about it saying..

)

This actor was left devasted after giving flops with Shraddha Kapoor, Katrina Kaif, begged for small roles; then...

The water cooler chat in most offices today would be about submitting the proof of tax-saving investments. Despite reminders from the Human Resource department most employees tend to wait till the last minute to do their tax-saving investments and hence there is a mad rush for such products.

Tax-saving mutual funds, technically known as Equity Linked Savings Scheme (ELSS), are a great last-minute option to save taxes. Besides good returns, ELSS investments allow for an exemption of up to Rs 1.5 lakh under Section 80C of the Income Tax Act. With nearly three dozen products in the ELSS category, retail investors could have a hard time selecting one. DNA Money talked with fund experts to come up with some easy tips for late-comers.

Lump sum or spread investments

Should you invest at one go or invest in small tranches? Nitin Shanbaug, senior group vice-president – investment products, Motilal Oswal Private Wealth Management said: "Investments in ELSS funds have to be held for three years as per regulations, post which an investor has the choice to either continue or redeem. Hence, it would be prudent that the choice of ELSS funds be made after proper analysis and investment be made in lump sum rather than trying to time entry over various tranches."

As ELSS funds have a lock-in period of three years, starting a Systematic Investment Plan (SIP) at this stage may defeat the purpose of investing, says Vijay Kuppa, co-founder, Orowealth. Investors must invest their money in one go, he adds.

Those with a few days to submit tax-saving documents, don't really have a choice of staggering their investments over the next two months. But not doing so could mean lower take-home for the next two months due to higher Tax Deduction at Source (TDS). Sanjiv Singhal, co-founder & COO, Scripbox says if the employer requires staff to submit investment proof in January or February, they will need to get proof that they have committed that investment.

But by investing in one shot for the short term, you lose the advantage of rupee-averaging, warns Aditya Bajaj, Head- Investments, BankBazaar.com.

If you are okay with getting tax refunds later, you may consider spreading the investment in ELSS funds. Kaustubh Belapurkar, Director - Manager Research, Morningstar Investment Adviser India says that investors can spread their ELSS investments over two to three tranches till end March, to reduce the risk of market timing. This can be done via the SIP route.

Even at the last moment, it is advisable to opt for a fortnightly SIP plan, to minimise risk, advises Saurav Basu, Head - Wealth Management, Tata Capital Financial Services.

Investors may evaluate investing in two to three funds instead of investing in only one fund. "Dividing the ELSS allocation will help investors manage risk emanating from any adverse performance or change of fund manager especially within the lock-in period," points out Devang Kakkad, Head Research, Equirus Wealth Management.

It would be best to stagger the investments over the next two to three months with a gap of 15-20 days, says Jason Monteiro, assistant vice-president - mutual fund research & content, Prabhudas Lilladher.

Investing in the last quarter of the year can inadvertently lead to investing at a higher price. "Our research shows that the average price of the S&P BSE 200 in the last quarter of the year has been higher in 15 out of the past 20 years when compared to the average price of the full fiscal year. Thus, those who invest in ELSS in the last quarter of the year, end up buying units at a higher price—resulting in a lower return on their investments," Monteiro added.

How to choose funds

Since ELSS funds are equity funds, investors should look for long-term consistent performance rather than recent returns, says Singhal and this requires a bit of effort.

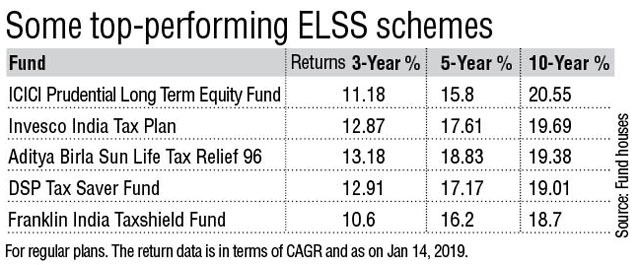

There are close to three dozen ELSS products on offer. Evaluating which fund to choose is an important task. While such investment is a guarantee for tax saving, there is no guarantee for higher returns unless you choose the right fund. For instance, the best three-year return is 19% CAGR for Mirae Asset Tax Saver, but the worst fund, that is, Union Tax Saver has given less than 8% CAGR in the same period ended January 14, 2019.

According to Kuppa of Orowealth investors must use their risk appetite in determining the best/ideal funds. "For example, Reliance Tax Saver Fund is a small-cap fund, while the ELSS by Aditya Birla is a large-cap fund. Thus, one should always do a thorough risk profiling before investing," he says.

If you are an aggressive investor, pick an ELSS fund which leans towards mid-caps. If you are a conservative investor, you may want to opt for a portfolio oriented towards large-caps.

There are other factors to consider. "Investors should identify the nature of the underlying exposure of the ELSS funds to ensure that the scheme objectives are in line with their own requirements. Also, each fund has a Key Information Memorandum and a Scheme Information Document, which investors must take the effort to understand," says Basu of Tata Capital.

Most investors when selecting an equity fund tend to focus on the recent performance. Simply looking at past performance over a fixed time frame is not the ideal approach, some feel. "A top performing fund today may not necessarily be a top performing fund tomorrow. Ideally, one should avoid funds with track record of less than three years and with an Assets Under Management of less than Rs 150 crore. Once the basic filtering is done, one needs to look at quantitative, as well as, qualitative factors when short-listing the right fund," said Monteiro.

Bajaj of BankBazaar.com believes the first thing to do is to look for consistent performers. "An ELSS product would have performed well in the last year, but if you dig deeper, you may find it underperformed the category average in the last four to five years," he says.

For instance, Canara Robeco Equity Tax Saver is the best performing ELSS in last one year, but its five-year return of 14.61% is lower than five-year category average of 15.7%.

There are some other metrics one can look at. "Investors can look at key parameters like (1) investment style of the fund manager (including market cap orientation), (2) time period for which the current fund manager has been managing the fund (longer the better), (3) consistency of performance across market cycles (at least three years) and relative to the peer group, etc," said Shanbaug.