An individual between 60-65 years and not having NPS account, can open NPS and continue investing till 70 years of age

The Pension Fund Regulatory and Development Authority (PFRDA) has decided to raise the entry age for National Pension System (NPS) from the current 60 years to 65 years. This is good news as it enables elderly in the age bracket of 61-65 to enter NPS. The big question is how will you benefit by entering NPS at this ripe age and how should you prepare. DNA Money spoke with top tax and personal finance experts to bring the pros and cons.

Scheme relevance intact: Tarun Birani, founder and CEO, TBNG Capital Advisors, says the scheme continues the option of making contributions up to the age of 70. So, someone who is currently 65 has five more years to accumulate wealth for this retirement planning. "The rationale for this revision in age limit was to widen the coverage of pensioners, currently serving only 15-16% of employees in India," he added. In this way, people can take advantage of NPS in case they are old. NPS is one of the lowest-cost pension product and a very efficient vehicle to provide old age income.

Suresh Sadagopan, founder, Ladder7 Financial Advisories, feels a little bit of more time would have really helped the late joiners. "It is welcome to allow people to join till 65 years of age. One does not know the motivation behind this move. But, joining around 65 may not serve the intended purpose as there is (practically) no time to accumulate a (big) corpus,” he says, adding that the present tax benefit for NPS could motivate some.

NPS as a tool: Senior citizens who are falling under income tax bracket can enroll in NPS and save additional tax up to Rs 50,000/- u/s 80CCD 1(B) till 70 years of age. "All other retirement schemes like employee provident fund (EPF), superannuation are linked to employment period and must be withdrawn at the time of retirement. But now, NPS gives opportunity to these retirees (having other sources of income) to invest further and build a corpus for higher pension at later stage," points out Rahul Parikh, CEO, Bajaj Capital.

With additional recent development of transferring superannuation funds to NPS, any individual completing superannuation age (between 60-65 years) and not having NPS account, can easily open NPS and transfer the funds and continue investing till 70 years of age. One-time transfer of superannuation funds to NPS is tax free. With increasing age expectancy and tax-paying senior citizens, PFRDA has opened another window for 60+ age category, added Parikh.

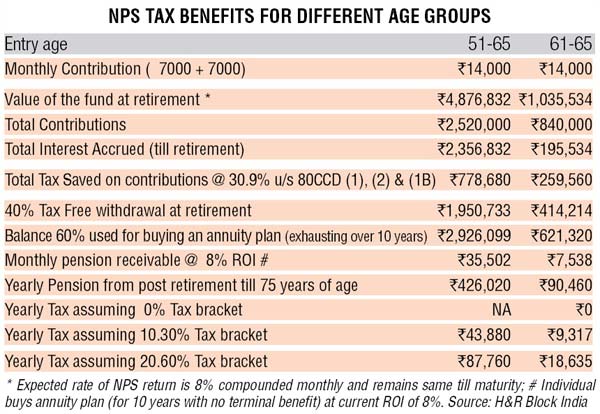

Tax on withdrawal and pension: Let us work with an example to understand NPS benefits for an aged individual during accumulation and withdrawal phases. People beyond 50 years of age are easily earning lakhs as monthly salary if not more, given their huge experience. Chetan Chandak, head of tax research, H&R Block India says that assuming gross monthly salary is Rs 1,75,000 and monthly basic is Rs 70,000, such a person as employee and his/her employer both contribute 10% of basic salary towards NPS (i.e. Rs 7,000 each per month, total yearly contribution of Rs 1,68,000). In this case, employee’s PF contribution and other 80C investment are Rs 1,15,800 as such he/she is able to take the entire benefit of NPS contribution every year. Assuming that NPS return gives 8% compounded monthly till maturity, and they withdraw 40% of the accumulated NPS balance and invest 60% in an annuity plan, there isn’t a huge tax incidence (see table). Till retirement the individual falls in 30% tax bracket and tax saving is calculated accordingly. Post retirement, tax rate applicable could be 0-20%.

Archit Gupta, founder and CEO, ClearTax also feels the tax implications on NPS investments remain the same for an investor, irrespective of when the investor starts to invest in the scheme. Investments of up to Rs 2 lakh in NPS can be used to claim deductions on income tax. This benefit is available to all NPS subscribers of all ages and income levels. Investors can use the entire NPS corpus to purchase annuity. There will be no tax implication on the amount used to purchase annuity, but pension that is earned from the purchased annuity will be taxable.

EVALUATING PROS AND CONS

- An individual between 60-65 years and not having NPS account, can open NPS and continue investing till 70 years of age

- Tax implications on NPS investments remain the same irrespective of when the investor starts investing, say experts

"NPS")

)

)

)

)

)

)

)

)

)

)

)

)

)

)

)

)

)

)

)

)