Rather than going for return of premiums plans, it’s better to invest in mutual funds or other savings products

It is human nature not to want to spend money without getting back something in return – a trait that extends to the insurance industry. Typically we don't like 'writing off' the premiums that we pay to get ourselves insured and seek policies that will return the premium to us.

However, on closer analysis, this may not always be a good thing and it's better to keep insurance and investment priorities separate.

"Term insurance – return of premiums plans (a variant of the term insurance plan) are seen as a sort of a 'zero cost' plan," says Sanjay Tiwari, director- product management and customer service, Exide Life Insurance. A concept under the term insurance spectrum, return of premium (ROP) insurance simply means that all the premiums are returned to the insured as maturity benefit. The product targets those looking for guaranteed cash value while buying an insurance plan.

CHOOSE RIGHT

|

- Insurance plans include pure protection plans at one end of the spectrum and assured return plans at the other

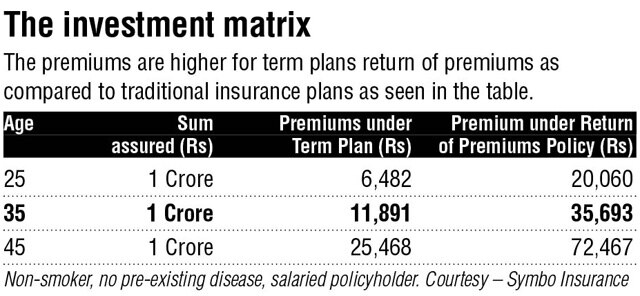

- Premiums are higher for term plans return of premiums as compared to traditional insurance plans

- To ensure hassle-free claim settlement policyholder should ensure complete and truthful disclosure

|

"Insurance plans include pure protection plans at one end of the spectrum and assured return plans at the other," explains Rushabh Gandhi, deputy CEO, IndiaFirst Life Insurance. Thus, a term plan with ROP is a combination of the above.

But there is no such thing as a free lunch and this extends to the insurance industry.

"Under this plan, the total premium payable includes the amount needed to cover the risk (cost of insurance) plus a little extra that is invested in safe instruments," explains Gandhi about the higher premiums under this plan vis-a-vis vanilla (traditional) term policy. The extra premium collected has to earn an adequate return to cover the cost of insurance. This structure enables the insurer to return the premiums paid if the death benefit does not get triggered.

But, at the end of the day, are the higher premiums under term insurance returns of premiums vis-a-vis simple term plans worth it?

"It's prudent to look at risk and investment decision in two separate buckets," says Anik Jain, co-founder and chief executive officer, Symbo Insurance. Your return on your investment depends on the opportunity cost of alternate investment options.

The return on investment for additional premium paid for the return of premium option would be in line with guaranteed return investment options. "It's fair to treat this portion of investment as a low-risk low-return option and take investment decisions accordingly," says Jain.

"We believe that if customers are looking at getting returns on insurance they should look at investing in ULIPs (Unit Linked Insurance Plans – a combination of investment and insurance) that gives one the advantage of participating in market-linked returns for building a corpus, and at the same time provides a financial security for the family to achieve their goals," says Dheeraj Sehgal, chief distribution officer – Institutional, Bajaj Allianz Life Insurance on how to plan your investments while having an insurance component in your financial portfolio.

"My suggestion is that rather than going for ROP plans, better to invest the extra money into other schemes such as MFs or other savings products," emphasises Rakesh Goyal, director, Probus Insurance.

Please remember that any life insurance policy can be seen as a combination of risk and investment options, but the percentage premium allocated to risk defines the policy structure. "A Pure term policy allocates 100% of premium to risk cover, ULIP policies allocate majority premium to investment whereas ROP policies allocate a majority to risk and minority to investment," explains Jain.

"I generally advise all my clients and team members to go for simple term plans for longer coverage preferably to the age of 85 years with maximum possible sum assured with a reputed brand, but not overly costlier," says Goyal.

So considering that term insurance – returns on premiums are probably not your best fiscal investment choice, why and whom should go in for them?

"These plans (return of premium) work well for first-time life insurance buyers who are uncomfortable about getting no (financial) benefit for surviving the insured term and might see the premiums paid as a sunken (lost) investment," says Tiwari.

Term plans – return of premiums plans may also be suitable for occupations with irregular income as they offer proportionately reduced benefits in case of non-premium payment, unlike a term plan which will simply get lapsed.

"Since traditional India is prudent with day to day expenditure and is conscious of quantifiable returns on their money spent, return or premium plans perfectly addresses their concerns," says Tiwari about the financial priorities of India.

Insurance policies offer tax benefits at both purchase and maturity stage under section 80(c) and 10 (10d). "Most policies are structured to be tax exempt at both purchase and redemption but it's prudent to check taxation benefit at the time of buying insurance and asking specific questions to the insurance company or advisor," says Jain.

Also, keep your paperwork in order for return on premiums like any other type of insurance product. Claim settlement ratios for life insurance companies are in the higher percentile and very few cases of claim rejection. The major reason for claim rejections for the term policy is incomplete or incorrect information provided by policyholder at the time of policy purchase. "To ensure hassle-free claim settlement policyholder should ensure complete and truthful disclosure," says Jain.

Minimum and maximum entry age of 18 and 65 respectively for ROP Plans. Critical illness and accidental death benefit riders are available and payment frequency allows flexibility of monthly, quarterly, six monthly or annual payments.

"Investments")

)

)

)

)

)

)

)

)

)

)

)

)

)

)

)

)

)

)

)

)