Balance of payment deficit may worsen this fiscal, force central bank to go for swap deal on FCNR (B) deposits

The recent free fall in the rupee, shrinking foreign exchange (forex) reserves and a possible balance of payment (BoP) deficit in the current fiscal, have economists wondering whether the government and the Reserve Bank of India (RBI) may look at a swap deal on FCNR (B) – foreign currency non-resident (bank) – deposits to stabilise the Indian rupee against the dollar.

The RBI had announced a similar measure in 2013, when it had opened a window to the banks to swap fresh FCNR dollar deposits to arrest the steep plunge in the rupee then.

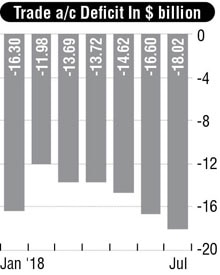

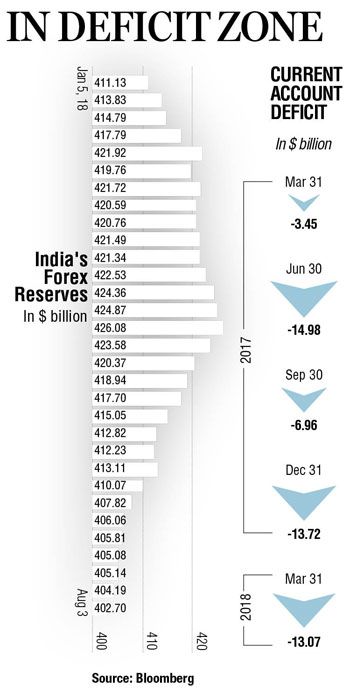

This year has already seen the rupee slip over 8% and touch 70.15 against the dollar last week. At the same time, forex reserve has depleted by $25.15 billion to $400.88 billion from the peak of $426.02 in April. Another worrisome macro data published by the government last week was that of trade deficit, which expanded by $18 billion in July and now stands at 8.1% of the GDP.

A report by financial services firm Nomura forecasts India's current account deficit (CAD) to widen to 2.8% of GDP this fiscal because of higher global crude prices, depreciating rupee and outflow of portfolio investments. Swiss investment bank Credit Suisse has also forecast net capital inflows at $55 billion to be lower than the projected CAD of $75 billion this fiscal.

A report by financial services firm Nomura forecasts India's current account deficit (CAD) to widen to 2.8% of GDP this fiscal because of higher global crude prices, depreciating rupee and outflow of portfolio investments. Swiss investment bank Credit Suisse has also forecast net capital inflows at $55 billion to be lower than the projected CAD of $75 billion this fiscal.

As all these adverse events come together, Devendra Pant, chief economist and senior director (public finance), India Ratings and Research (Fitch Group), foresees the need to mobilise foreign currency investible resources to check the sharp drop in the rupee value against dollar this fiscal.

"Capital inflows or the portfolio investments have not been that strong and the current account deficit has widened. Therefore, we could see a deficit on the balance of payment. We believe the government and the RBI, together, will go for NRI deposits, something similar to 2013, to the tune to $25 billion this fiscal to stabilise the rupee," he said.

Pant said the $25-billion FCNR (B) deposits could stabilise the Indian rupee at an average of around 68.40 per dollar or else it could just scale to higher levels.

"The moment you do the $25 billion FCNR (B), you may see the balance of payment's capital account inflows higher than your current account," he said.

The India Ratings and Research economist's estimation is based on a CAD of 2.6% of GDP or $71 billion. Pant calculates that at that CAD level, the trade deficit would be somewhere around $19.5 billion or 7.3% of GDP. And with capital inflows falling or in the negative, the BoP could slip into deficit zone.

The India Ratings and Research economist's estimation is based on a CAD of 2.6% of GDP or $71 billion. Pant calculates that at that CAD level, the trade deficit would be somewhere around $19.5 billion or 7.3% of GDP. And with capital inflows falling or in the negative, the BoP could slip into deficit zone.

"Foreign portfolio investments (FPI) have been negative. It's only in July that the FPI investment picked up but there is already a hole in the entire year's capital flow. The FDI is there but it is not that much that it will able to compensate for higher trade deficit because of oil prices. Today, the government has come out with the estimates of import bill being higher by $26 billion. Out estimate of that is anything from $23 billion to $30 billion. So, we are looking at an all-time high trade deficit this year," he said.

The trade deficit was at $13 billion or 6.3% of GDP last fiscal. In 2012-13, it had soared to 10.5% of GDP, which had knocked down the rupee to record lows.

The trade deficit was at $13 billion or 6.3% of GDP last fiscal. In 2012-13, it had soared to 10.5% of GDP, which had knocked down the rupee to record lows.

D K Srivastava, chief policy advisor, EY India, said a BoP deficit could be expected in the current fiscal and feels foreign exchange investible resource mobilisation exercise should be undertaken on a regular basis to avoid currency volatility.

"That (BoP deficit in the current fiscal) is to be expected. We should try and attract investible resources in foreign exchange terms by whatever schemes we can and utilise it for infrastructure and other investments," he said.

Rishi Shah, economist, Centre for Digital Economy and Policy, also believes the current fiscal could see a BoP deficit but said would like to wait for some more time before making an authoritative comment on it.

"We can have a year wherein overall BoP is in deficit. But it is too early to say anything on that as there is still a very large part of the year which you have to go through. Let's see how the overall global economy behaves," he said.

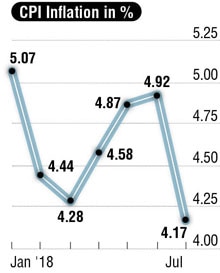

EY's Srivastava saw drying up of forex reserves as a temporary phenomenon; "once all these tariff actions and reactions settle down, most of these things would settle down. My take is those economy which maintain better macroeconomics, includes fiscal deficit, inflation profile as well as CAD. Our CAD at sustainable level would be about 2.4-2.5%. Inflation (went up) only seasonally but is under control. On the fiscal deficit front, there is a slight slippage but it is not excessive compared to other emerging market economies".

Shah said only if India were to lose another $20 billion of its forex reserve, it would become a concern.

According to him, based on an average import of $40 billion per month, the current $400.88 billion forex reserve gave a 10-month cover.

"Generally, when you have more than a year's worth of reserves it is a good position to be in. But 10-month import cover is also comfortable. This is a crude measure, you are always exporting something also. We were always around the 8-month import cover most of the time. Right now, we are in a better position," Shah said.

The EY economist also does not see rupee at 70 levels as a major concern as it was expected to fall to that level and then stabilise. According to him, since India's inflation rate was higher than US's inflation rate, the rupee was bound to depreciate vis-à-vis dollar

"(Rupee) should have been depreciating like that (in the past) but it started to appreciate. So, I think 70 would be considered a regular level, considering differential inflation rate (between India and the US) but beyond that, it would be a concern," said Srivastava.

"NRI deposits")

)

)

)

)

)

)

)

)

)

)

)

)

)

)

)

)

)

)

)

)