Banks undertaking Rs 100-200 crore one-time settlements in small value accounts every quarter

Banks are going for one-time settlement (OTS) of debt as they fear that economic slowdown may be prolonged and crimp borrowers' ability to repay loans.

Though it is difficult to put a figure to the loans settled under OTS for all lenders, each bank is undertaking Rs 100 crore to Rs 200 crore of one-time settlements every quarter.

Depending on the size of the bank, OTSs are taking place from accounts with an exposure of up to Rs 300 crore. For most banks, it is more of a policy for small value accounts.

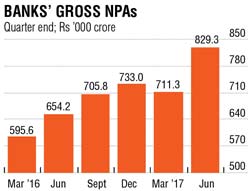

The menace of non-performing assets (NPAs) continues to haunt banks, with two rating agencies raising concerns on the pile-up of bad assets and lenders’ failure to recognise them. While domestic agency Crisil forecast a spike in NPAs to 10.5% of total loans by March and the system level stress at Rs 11.5 lakh crore, or 14 %, its global rival Fitch placed the banking sector under a negative outlook. Crisil said since banks have only recognised two-thirds of their stressed loans as NPAs "bad loan ratio is set to rise by 1% to 10.5% by March 2018, up from 9.5% in March 2017, which included only two-thirds of the overall stressed assets."

In the past, OTS was limited to a few cases. Now with the economic slowdown persisting and cash flows of promoters getting strangulated, banks are preferring to have a bilateral settlement where part of the money comes back to the bank.

For banks like State Bank of India (SBI), the value of exposures closed due to one-time settlement in some cases is high as t Rs 300 crore. For most banks, OTS is a policy whereby accounts of a certain size are closed.

A senior SBI official said, “We have undertaken OTS for exposures up to Rs 300 crore where the underlying security and the net present value of the asset is calculated to arrive at a settlement value. The haircut or the interest foregone will be about 20% to 25% depending on the securities and the age of the accounts. It is done mostly for accounts where there is a single exposure and promoters are willing to revive the company after settling the dues. All small-value accounts that are stressed we will look at one-time settlements.”

Private banks are insisting payment at one go during the OTS rather than staggering the payment.

A senior Federal Bank official said, “We would have done close to Rs 180 crore of OTS in the first quarter. In many cases, these are fully provided for accounts so after the OTS we are able to write back our provisions to the profits.”

Usually, when a loan is not repaid in 90 days it turns into an NPA and the bank has to keep aside capital for it. If provisions are high then after OTS the bank can add the capital kept aside as a buffer to its profits.

IDBI Bank is another lender which is aggressively driving the OTS policy in all its zones and branches, taking a small haircut and closing accounts wherever possible irrespective of the sectors.

A senior IDBI official said, “One-time settlement is not a policy across sectors wherever there are small value accounts of up to Rs 30 lakh, we do a one-time settlement. For exposures up to Rs 10 lakh, the haircuts are larger because the borrower would have genuine cash flow problems and may not have enough to pay. In higher loan amounts we take lesser hits taking into consideration promoters may have other sources of funding.”

...& ANALYSIS

- For big banks like State Bank of India, the value of exposures closed due to one-time settlement is about Rs 300 crore

- IDBI Bank is aggressively driving the OTS policy in all its zones and branches, taking a small haircut and closing accounts wherever possible irrespective of the sectors

"Money")

)

)

)

)

)

)

)

)

)

)

)

)

)

)

)

)

)

)

)

)