Reported By: | Edited By: N S Venkatesh |Source: DNA |Updated: May 14, 2018, 05:35 AM IST

| Edited By: N S Venkatesh |Source: DNA |Updated: May 14, 2018, 05:35 AM IST

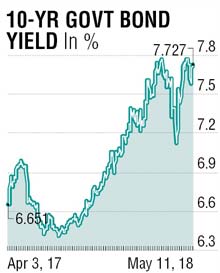

Another edge-of-seat kind of week passed and investors and traders have already spent a third of the year wondering where the markets are headed. Oil surged as Iran deal scrapped and the US inflation reading came in bit tame so bonds recouped some losses. The global equities showed solid advance during the week. Irrespective of all these, Indian bonds continued to suffer losses as another auction, the fourth in succession had a large devolvement. Volatility, as measured by the CBOE’s Volatility Index (VIX), declined to 13.1 from 15.2 a week ago.

The nemesis of market participants in recent months, crude oil, extended gains amid fears and repercussions of Iranian sanctions by the US. WTI crude rallied as high as $71.79 a barrel this week in the wake of the US President Trump’s move to pull the US out of the Iran nuclear agreement.

Unless a new arrangement is made, sanctions will begin to be reimposed on Iran in the next 90 to 180 days. Iran’s regional rival Saudi Arabia says it will work with others to mitigate any potential supply shortages. Tensions between Iran and Israel ratcheted up further this week, with Iran firing rockets into Israeli territory from Syria, prompting Israel to strike back.

In other developments, attempts by Argentina to stem capital outflows proved insufficient this week, prompting its government to turn to the IMF for help. Talks are now underway with the IMF, and any support package will likely require faster fiscal consolidation. The long-term players will not miss recalling which of the past events will redux – LatAm debt crisis of 1982, Savings and Loan crisis of the 1980s, Asian Crisis of 1997-98 or the most recent GFC of 2007-2008. Each episode of ultra-easy liquidity and lower rates have been followed by a shakeout that leads to an EM crisis. The US CPI rose less than expected in April, suggesting that inflation was increasing only at a moderate pace, which may possibly lead the Federal Reserve to follow a gradual path after a priced-in June 2018 hike.

Indian markets continue to be a conundrum of sorts. An open market operations (OMO) announcement did not help markets beyond a knee-jerk rally and with yet another auction; the fourth in a row, devolving on Primary Dealers, the message is loud and clear – total lack of demand and fear of further losses in books. It appeared to be a case of yielding to popular demand that the government needed to have more issuances at the shorter end of the curve. However, the response to auctions suggests differently. Sustained and large quantum of OMO purchases may be required to correct the already inverted curve.

March Industrial Production data came in at 4.1%, lowest in past five months with a sharp downturn in the capital. Inflation numbers for April, to be announced today, is expected to be showing a higher reading. Well, this is already priced in. Given the current trajectory of inflation and the likely second-round impact from crude-led inflation, it still doesn’t merit the pessimism that is seen in yields and sentiments.

Circa 7.80% has held the top on a few occasions in the past, with regard to the benchmark 10-year bond. Expect this to hold. A combination of aggressive OMOs at the shorter end and the rupee stability will be key to any change in market confidence. A 7.80-7.65 range for the week expected.

The writer is a market expert