Reported By: | Edited By: Amar Pandit |Source: DNA |Updated: Sep 17, 2018, 06:05 AM IST

| Edited By: Amar Pandit |Source: DNA |Updated: Sep 17, 2018, 06:05 AM IST

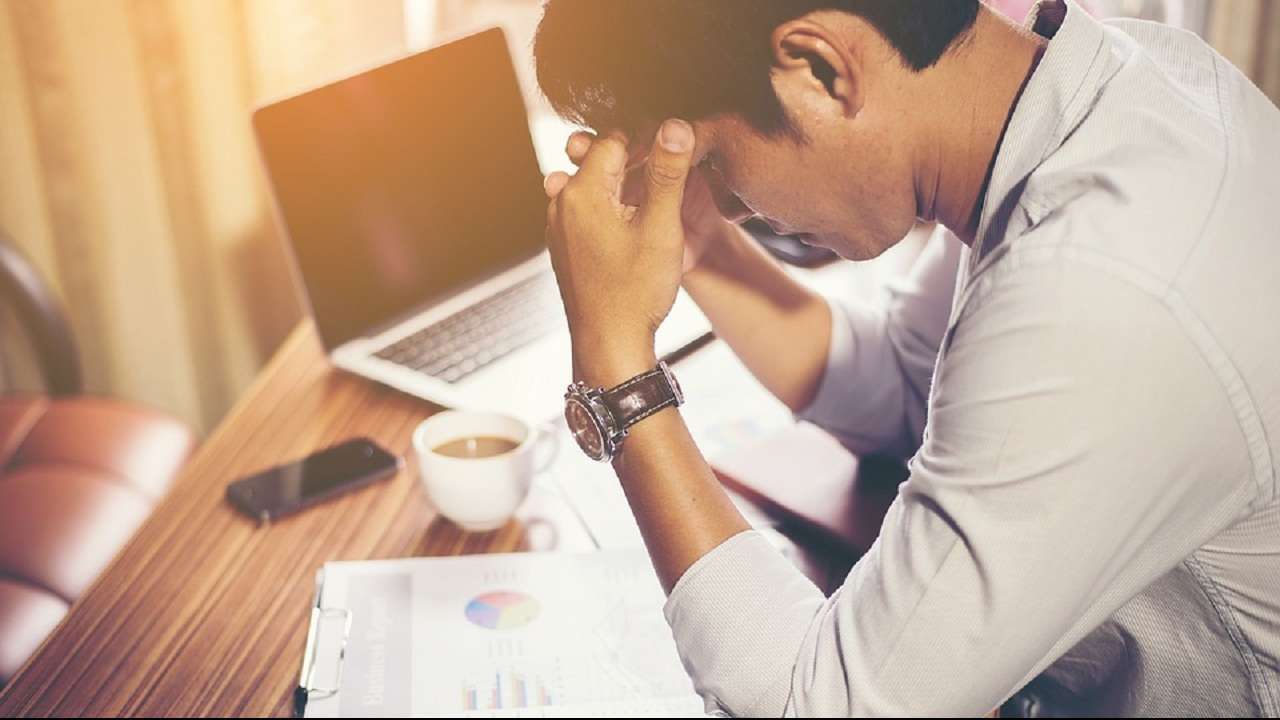

Studies globally identify money as one of the top causes for stress. As society equates wealth with success, people going through financial issues often feel incompetent if they do not have enough money to show, or frustrated if they are unable to provide well for loved ones.

Here are four common mistakes that make one vulnerable to financial stress, but can easily be avoided:

Household income levels in our country are rising, and many young families have double incomes. On the flip side, saving as a virtue is becoming old fashioned. Unlike the previous generation that held savings as a virtue, the current generation is oriented towards consumerism. Yet the truth is, most of us can live on less than we think we can. So, the magic mantra to adopt is: switch to a savings budget instead of the expense budget. Save adequately and spend the rest guilt free.

Too much debt can spell trouble for anyone, but especially so for business owners. Leverage may be a good idea for financing your house, car or business. However, the key lies in knowing how much debt you can comfortably take. Your actual EMI affordability can be quite lower than what your bank thinks you are eligible for, because loan eligibility calculations typically look at your aggregate income and assets, but not how you actually spend.

The risk of financial distress in the event of hospitalisation can be mitigated through appropriate insurance covers. With advancement of medical technologies, the cost of medical care is sky rocketing by the day. A single hospitalisation can leave a gaping hole in one's savings kitty. Cover the entire family with a good health insurance policy. If you are earning and have dependents, having a life cover is mandatory. The life cover should be sufficient to take care of your dependents' needs, and your liabilities, if any, until the dependents can provide for themselves. Buy a pure term policy, skip traditional plans and Unit Linked Investment Plans.

A gentleman recently recounted about his son who had to skip work for over a month to take treatment for back and leg injuries, he got during a football game session with colleagues. Luck sometimes goes the wrong way; a job loss or a prolonged illness. Having a rainy-day fund eases the stress of such situations. Make a detailed cash flow statement listing down all expenses incurred monthly. Multiply that by six. Contribute towards this corpus gradually by investing in a liquid fund and don't dip into it for anything other than emergencies.

In urban settings, where the demands of work life and commute is often overwhelming, a lot of otherwise smart and successful people end up doing poorly with finances. A remedy for this is having a good financial planner or coach. A coach would not only help you focus on goals and align investments with those goals, but would also help you cultivate a healthy financial behaviour.

Identify a good financial planner, someone who is qualified for the profession. Don't be carried away by brand names, especially of banks, and don't believe your relationship manager, chartered accountant or insurance agent can double up as a good planner.

Focusing on avoiding the four mistakes of financial behavior discussed above and consulting a good financial planner can go a long way in helping you keep financial stress at bay.

The writer is founder and chief happyness officer at HappynessFactory.in