Reported By: | Edited By: R N Bhaskar |Source: DNA |Updated: Mar 19, 2018, 03:28 AM IST

| Edited By: R N Bhaskar |Source: DNA |Updated: Mar 19, 2018, 03:28 AM IST

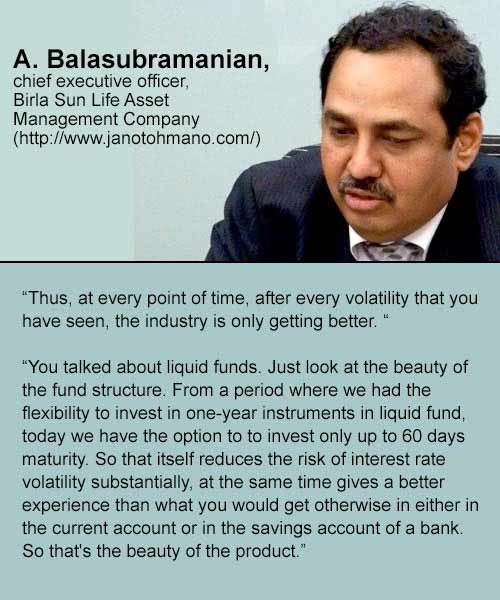

And it also comes with the least possible expenses, where the expense ranges from 20 basis points to 40 basis points. It moves along with the overnight rate that prevails in the market.

Short-term rates are high because it is also a beneficiary of the liquid fund, except the volatility which you'll see at an intermediate period is for now two days.

But that doesn’t mean that there is a significant amount of risk that exists. This is because most liquid funds do not invest in more than 60 days maturity. The same time they do not have instruments having average maturity of more than 25 to 30 days in a normal course actually. So that's the beauty of this product.

DNA: What about gold ETFs. Will that die out?

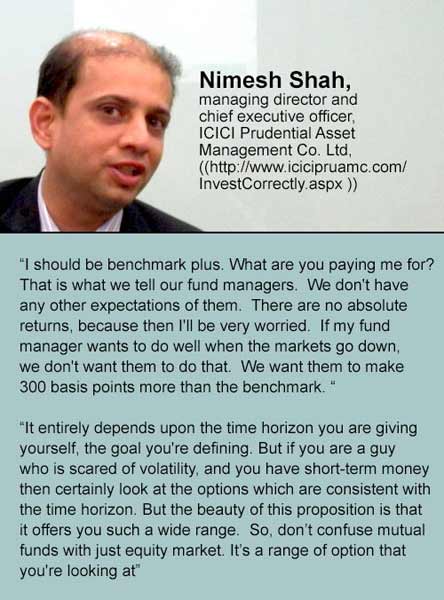

Shah: Lots of AMCs had gold funds…

People who wanted to allocate money towards gold would have allocated that. So that investment phase is complete. So whoever has allocated money to such funds is still out over there.

DNA: But fresh money won't come in, right?

Shah: Right. So, a lot of money today is is instead coming into FMPs. Investors have also become smarter. I'll tell you what they are doing. There are some value funds in the market. People understand that when the markets are down, it means that mid caps have been beaten up. Investors have become much smarter, They understand that there are some stocks in the market which are going quite cheap. On the liquidity side the market is very cheap if you remove the top 12 stocks.

So the rest of the market being cheap, there are a lot of people who are coming into value funds, right. So the movement is happening. Volatility is here to stay. So people are coming into a set of funds which gain out of volatility.

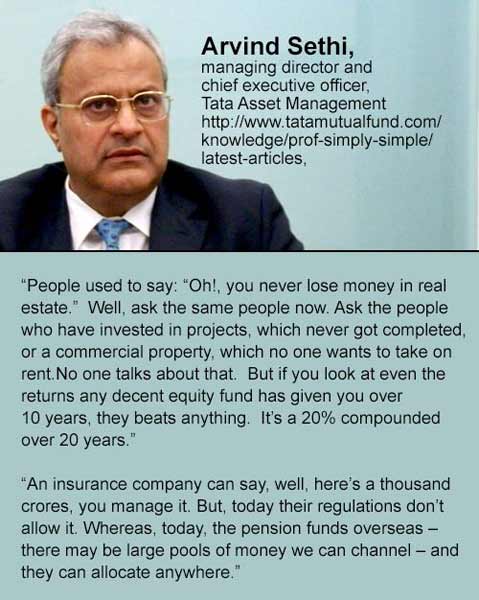

Soni: I think the investment in gold ETF was a very small portion of mutual funds. It was less than 1% of the industry, in fact it was like Rs.8,000, 10,000 crores…

Sethi: It’s just about Rs.4,000 crore…

Soni: So, a very small portion of the industry and investors actually favored other products like debt or equity mutual funds a lot more.

Sethi: But look at the beauty of the industry. Supposing we wanted to hold gold, what were your choices? And provided you had accountable money as well? You could have bought physical gold and run the risk of storing it somewhere in your house or in the vaults; or you buy it in an ETF. Now even if you wanted to buy physical gold, who would you buy it from? What would you end up buying? Would you get the purity? Plus there will be minimum bar sizes that you have to buy. Here you can put Rs 1,000 rupees in gold.

DNA: Yes. There was greater flexibility.

Sethi: But look at the safety. If you wanted to play this five times as the price moved up and down during the last 10 years, you had a choice of going to your jeweller and buying something. But here you can do it safely through a fund, you write a cheque out, and it comes to you. You don’t have to worry about safety, insurance, etc.

What I'm saying to is that that sort of flexibility, range and convenience the mutual fund provides, whether it’s for debt, whether it’s for gold, whether it is for equity. Or if you think you are smart enough, you can do your own financial planning.

Then you say, I'm going to put X per cent in equity, Y per cent in debt so on and so forth, and then you come to the mutual fund industry which has this menu of different equity funds, debt funds and liquid quasi debt funds. And that’s the way to use and think about mutual funds. It is like having a good GP who is your adviser. We are the ones who produce the pills. So if he says you need something for a headache, and here is a pill for a headache. You have to ensure that you get quality pills, or you could be getting something which is adulterated or which is contaminated.

And look at the flip side, so if I may. Look at the real estate industry. One of the biggest investments people make is in their house. Before the project is even launched, some broker calls you up. You’ve not seen it. You don’t have any offer document to say what it is. You write out a huge cheque. You have no idea what timelines are going to be adhered to. You don’t know how he is going to change the building plan even. And yet people go and put all their money and faith into that.

And here the indust4ry is a very regulated, very transparent one, which is trying to do a good job, is run by professionals and people stay away from it – I mean it’s unbelievable.

Shah: Another area where a lot of money goes, I believe is in international investments. A lot of fund houses have got this option as well. When we manage, we invest in equity in the country. There is also an option to invest in equity outside the country. So say if you've got expenditure planned in foreign exchange, this may be an option. There are people who say that “we've got expenditure in dollars over a period of time -- son’s education expenditure, daughter’s education expenditure -- which is outside the country. Then you can lock into your dollar business -- dollar at that point of time. So, a lot of people have started investing in international funds. Investing across the world.

DNA: Those who invested in foreign funds must be laughing their way to the bank, considering the rupee's fall. . .

Shah: And the ease of doing this is by writing a cheque…You just fill up – or someone fills up – a form.

Soni: But it is very difficult to explain this to people that’s why you [the media] have to do this…

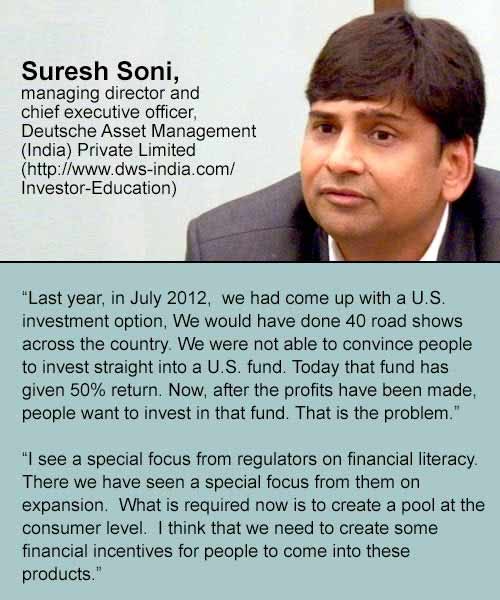

Last year we had come up with a U.S. investment option -- just one year ago, in July 2012. We would have done 40 road shows across the country and I myself did 30 road shows across the country. We were not able to convince people to invest straight into a U.S. fund. Today that fund has given 50% return. Now, after the profits have been made, people want to invest in that fund. That is the problem.

The whole challenge is convincing people about an idea in the first stage when it is in an idea mode, where the returns are not coming.

Balasubramanian: Just prior to what Nimesh mentioned, we launched an international equity fund too with the help of S&P. It’s exactly about five years ago. But in an emerging market investment from a global investor's point of view was gaining momentum. And the whole investment was post the announcement of RBI that up to $200,000 could be invested overseas. So, we launched that fund. 65% of the money is invested in the U.S. equity and roughly about 10% of money invested in developing or developed markets. It is five years since then. It has met its benchmarks. But two and half years ago, there were people who were getting impatient. And incremental money did not come in.

Shah: We were not able to convince people. But that’s probably true of virtually any investment.

Balasubramanian: Any investment.

Shah: It’s not that. It’s not only about investing in the U.S. dollar. It is about investing in businesses which are not available in India. If – when you invest outside the country – you might get investment into airline companies, you might get investment into cola companies, which supply across the world.

So, a lot of stability can be possible – global companies, which are present in countries across the world. That itself offers stability of revenues.

So, if India is volatile this opportunity makes sense. If you see the last five years, two years India was at the top in terms of giving returns and two years we were at the bottom, right. So, we are either at the top or we are at the bottom as far as the worldwide returns are concerned year-on-year. So, this kind of international investment gives stability to part of your portfolio.

DNA: Brilliant.

Soni: When I started the discussion, I talked about financial literacy. Indeed, one of the things that is happening over a period of time is that regulators are addressing all these issues one by one. So I see a special focus from regulators on financial literacy. There we have seen a special focus from them on expansion.

What is required now is to create a pool at the consumer level. While we can very easily say is that, well, the consumer pool will come and they’ll make money, I think that we need to create some financial incentives for people to come into these products.

DNA: Yes.

Soni: So right now, I think if you really see the tax incentives that are available for mutual funds, it’s just a part of that ELSS [equity linked savings scheme] thing, which has stayed at the same number for -- I don’t know how many -- 15 years plus probably. So if you can create some kind of tax incentive for people for investing long-term money -- and it need not be short-term, it can be long-term money -- then it can become a part of the investment plan.

DNA: It will incentivise people to look at mutual funds.

Soni: We have seen the impact of these tax incentives and the other schemes that are announced periodically. Therefore, if some kind of incentive can be created, it can be really helpful.

So while the industry is working on its own to reach out, create awareness, create demand for the products, this just can come in handy.

DNA: That’s a good idea. Any other ideas that you think the government should consider.

Balasubramanian: Another recommendation that has gone from the industry -- this has been pending for quite some time -- is on the lines of 401(k) in the U.S. It is a defined contribution towards investing in mutual fund product and -- which is like our provident fund -- that’s also comes as part of the salary income as a defined contribution towards mutual funds. If and when it comes, it will really increase the penetration of MFs in India. It will also bring into play a large pool of stable domestic retail money.

DNA: Regularly. Almost like a recurring deposit.

Balasubramanian: Correct. It would also help create a vibrant capital market and also expand the industry’s customer base. Today the customer base is somewhere around 3.8 crore to 4.2 crore.

Soni: Something like this is available in Singapore as well. You could easily say that I want to put this money into fund A so much, fund B so much and then every month it keeps on getting deducted. So it becomes a habit.

Shah: In effect, what they are saying is that today we don’t have a proper institutional market. Overseas insurance companies, pension funds can also give their money to be managed by a mutual fund, to an asset manager. Whereas here – because all the regulators are in silos. And I think some regulation there would certainly put more money available for this industry, and also create a genuine institutional market.

Sethi: An insurance company can say, well, here’s a thousand crores, you manage it.

Today their regulations don’t allow it. Whereas, today, the pension funds overseas, there may be large pools of money we can channel – and they can allocate anywhere.

DNA: So that flexibility in regulation is required.

Shah: In the last five years the industry has grown, and now the product is quite beautiful. It is still a challenge for us to reach the final customer. It is a push product. But we have to make it a pull product, so that the customer should be asking for that product. Only two things can bring that pull.

Either there is a tax advantage of investing in mutual funds. Anywhere in the world; mutual funds have grown because either pension money have contributed to their growth, or the granting of tax advantages for investing in mutual funds. If one of the two things happen, it will be great for capital formation and also for the country.

If we need capital formation in this country, we need people to be enthused to invest in capital.

That is when the mutual fund industry will become more relevant. Till then we’ll keep on pushing.

And we have to work with the various media companies, so that we reach the final customer. It is to make him financially literate.

It is, therefore, very important to work with publications as yours, to reach the final customer.

DNA: Are the regulators sympathetic and positive towards such recommendations?

Balasubramanian: We have already submitted this as potential gaps that need to be filled, for the growth of industry.

The reception was pretty good, and given the fact that, at the country level, we have many challenges to handle the fiscal exercise. But I am confident it will come – even if gradually.

Shah: We have created a great product in the industry. Now we should go all out and reach the final customer more and more, and grow the industry and help investors invest better. We have to ensure that savings get converted into investments. Good for the country. Good for the individual.