Reported By: | Edited By: Mohan Shenoi |Source: DNA |Updated: Dec 18, 2017, 01:35 AM IST

| Edited By: Mohan Shenoi |Source: DNA |Updated: Dec 18, 2017, 01:35 AM IST

Year 2017 is now ending with global asset markets at multi-year highs amid a “Goldilocks scenario” of accelerating growth, low inflation, collapsing market volatility but also a swing toward right-leaning politics. Other positive global catalysts were supportive fiscal policy and till recently an accommodative monetary policy. This was supported by the resolution of the first phase of the EU-UK Brexit withdrawal deal and progress on the US tax reform thus, negating the North Korean provocations.

This positive context is expected to continue into 2018 with synchronised global growth (out of stimulative US fiscal policy) and moderate political risks. However, the negatives could come from a sudden rise in inflation out of higher fuel prices, tight labor markets and persisting growth. Absent an external shock, major global central banks are also likely to continue with non-disruptive normalisation of monetary policy, with only Japan maintaining its “yield curve control” framework.

In early 2018, the formation of the German coalition, Spain’s Catalonia issue and possibly Italian elections will dominate the political landscape. Later in the year the mid-term US elections and the ongoing UK-EU Brexit talks will influence markets.

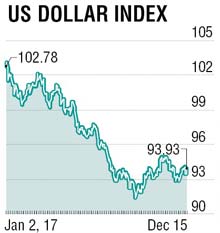

Globally, we expect the US dollar to retain its strength at least in the early part of the year with new non-Economist leadership of the US Federal Reserve (Fed) and a favourable macro backdrop driving the pace of future rate hikes (already 125 basis point since December 2015). The euro will attempt to balance political uncertainty with a data dependent removal of accommodation. The Bank of England (BoE), and so the pound sterling, will negotiate the tight-rope of balancing control of currency weakness-led heightened inflation with the twists and turns in the Brexit negotiations.

Globally, we expect the US dollar to retain its strength at least in the early part of the year with new non-Economist leadership of the US Federal Reserve (Fed) and a favourable macro backdrop driving the pace of future rate hikes (already 125 basis point since December 2015). The euro will attempt to balance political uncertainty with a data dependent removal of accommodation. The Bank of England (BoE), and so the pound sterling, will negotiate the tight-rope of balancing control of currency weakness-led heightened inflation with the twists and turns in the Brexit negotiations.

Elevated valuations will restrain incremental upticks in stock markets while yields are expected to tighten in line with policy moves. Commodity prices will rhyme to policy tightening, slowing credit growth in China and the adherence of oil producers to supply cuts as well as US supply growth.

The rupee appreciated in 2017 gaining 7% from 68.3450/U$ to 63.56/U$ with ample capital flows into asset markets, enthused by the reformist agenda and Moody’s commendation of the same, overwhelming a modest current account deficit (1.2% of GDP).

This resulted in a bulge in Reserve Bank of India (RBI)’s forex reserves ($32 billion, so far) to $400 billion in FY2018 as RBI intervened to prevent further rupee appreciation. The subtle hawkish tinge to the central bank’s “neutral stance”, hardening inflation (food and fuel related), uncertainty around the State election results and expected fiscal slippage, out of GST-related shortfall, has caused 10-year government yields to peak beyond 7.25%.

In 2018, as the economy tries to grapple with the GST-led disruption and the impact of US tax proposals, the rupee is expected to trade largely in the 63.50-66.50/$ range. There could be unsustained thrusts in either direction, out of capital inflows or geopolitical issues, but would be tempered by covert intervention.

The writer is president and chief operating officer, Kotak Mahindra Bank