Reported By: | Edited By: Pankaj Ghemawat |Source: DNA |Updated: Nov 21, 2013, 01:44 PM IST

| Edited By: Pankaj Ghemawat |Source: DNA |Updated: Nov 21, 2013, 01:44 PM IST

Six years ago, we saw not only the first publication of DNA, but also of Tom Friedman’s The World Is Flat. The book is worth revisiting because it was motivated by the Indian information technology (IT) sector, it had extraordinary impact at the time of its release, and it continues to have a strong grip on people’s imaginations.

Thus, in a recent Harvard Business Review blog posting, I ran a survey asking which of three quotes about globalisation came closest to mirroring readers’ views. More than 60% of the respondents picked the following apocalyptic pronouncement from Friedman over two more moderate alternatives:

The world got flat…[creating] a global, web-enabled playing field that allows for…collaboration on research and work in real time, without regard to geography, distance or, in the near future, even language.

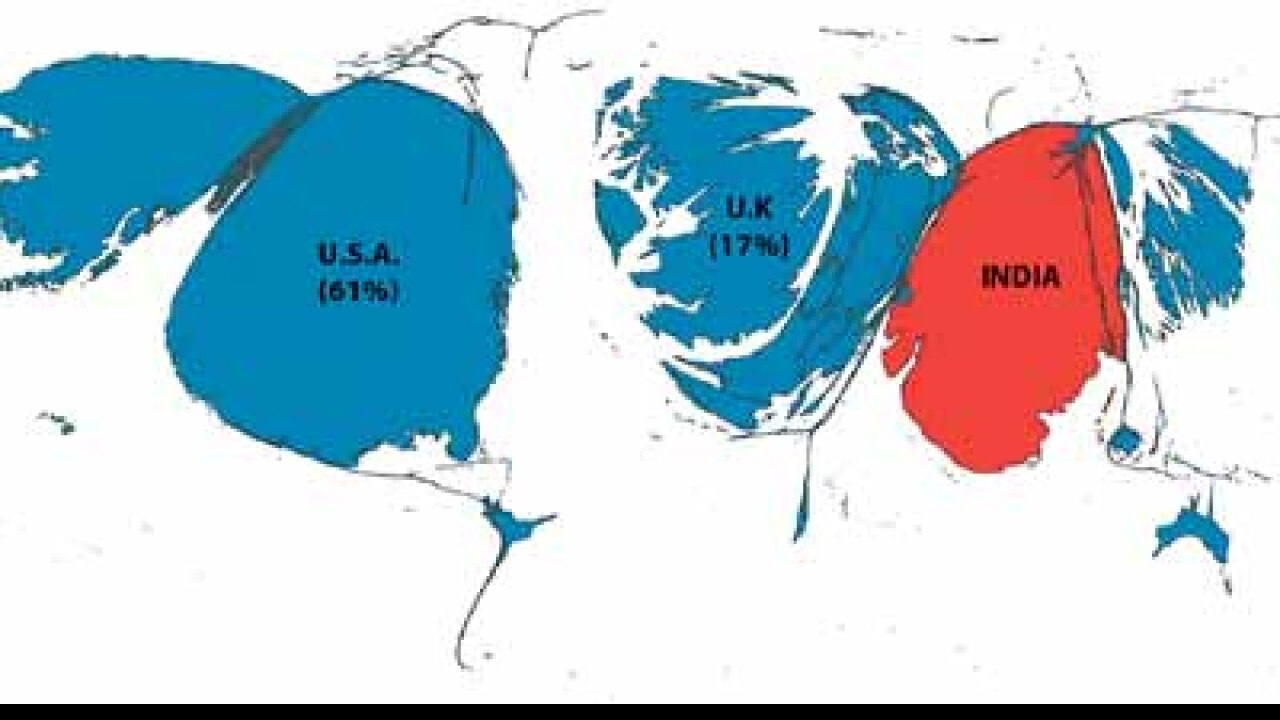

So how flat is IT services, Friedman’s favourite example?

The following maps, drawn from my new book, World 3.0, and updated, provide a visual characterisation. The map on the top of the figure shows countries proportional to their total spending on IT services. The map on the bottom, in contrast, sizes countries on the basis of their purchases of Indian IT services.

If the world really was flat, the maps would look similar. What the contrast between them indicates is that linguistic distance still matters greatly in IT services — hardly a surprise to anybody who has actually thought about what is involved in coordinating with clients to write custom software, manage and maintain computer systems, and the like. Nearly 80% of India’s IT exports go to the US and the UK, whereas Japan and continental markets are much smaller than the map on the top.

And I should add that years of efforts to diversify India’s IT services export destinations have not really changed the basic pattern. In fact, according to the latest report from Nasscom, the US share of Indian IT and BPO exports actually increased in the last fiscal. Furthermore, the burgeoning of the Indian domestic market can be seen as actually increasing the share of English-speaking markets in the total.

Why have continental Europe and Japan proven such hard nuts for Indian IT companies to crack? More than 95% of the personnel employed by Indian IT companies are Indian — although some of the larger firms, such as TCS, do better on this measure — and very, very few of them speak French or German, let alone Japanese. But the cultural issues go beyond language: these are markets that seem to require natives in marketing positions in particular.

Then there are administrative barriers as well: employment protection and other legislation complicate global sourcing in continental Europe and Japan. And as the visa-related issues in the US experienced by Infosys in particular indicate, even markets relatively (but far from completely) open to Indian IT companies can backslide.

Geography also seems to matter. As the Nasscom report notes, “With changing buying patterns, there is a shift towards using more local or near-shore resources.” Considerations related to time zones and risks as well as shared languages and administrative facilitation (eg: The European Union membership of many of the east European near-shoring destinations) all seem to play a role — but none of these would matter in a flat world.

Economic differences still matter as well — and one of them continues to be the major driver of the Indian IT industry’s continued success. Despite double-digit increases in recent years, Indian salaries for software programmers have increased from perhaps only 12% of US levels to about 20%. In a flat world, one would have expected wage convergence by now.

And there are also economic differences that present problems for global sourcing, such as currency volatility. While 2011 has (so far) been a relatively quiet year in terms of the rupee/dollar exchange rate, the average volatility of that exchange rate in the three previous years (2008-10) was nearly four times the level of the three years prior to the launch of DNA. (2003-05)! In this respect, among others, the world seems to have gotten less rather than more flat!

For all these reasons, when I did a keynote speech at the Nasscom summit in 2009, rather than soothing the audience with talk of flatness, I used my CAGE (cultural-administrative-geographic-economic) framework for thinking about differences to highlight the challenges facing the industry—challenges that must be recognised if they are to be addressed. I would still do that today.

And given what is going on in with the world—the prospects of unemployment in advanced economies fuelling xenophobia and administrative restrictions on global outsourcing, the increased emphasis on near-shoring, and uncertainty about the US dollar and its status as the world’s reserve currency — I can’t see that changing in the next six years, or the next twelve.

— The writer is professor of strategic management at IESE Business School in Barcelona, Spain and author of World 3.0: Global Prosperity and How to Achieve It, published by Harvard Business Press.