Reported By: | Edited By: Mohan Shenoi |Source: DNA |Updated: Nov 20, 2017, 07:25 AM IST

| Edited By: Mohan Shenoi |Source: DNA |Updated: Nov 20, 2017, 07:25 AM IST

This month, major central banks refreshed their monetary stances, US Federal Reserve (Fed) got new chair, House/Senate Republicans introduced their own tax proposals and India got upgraded. Politically, Japanese PM Abe won a resounding election victory; Spain broke down the Catalan separatists while Saudi Arabia’s King Salman asserted himself.

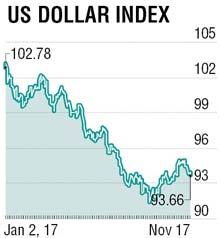

European Central Bank (ECB) left rates unchanged but halved asset purchases to eur 30 billion per month while extending the end-date to at least September 2018. The euro swooned to U$ 1.1553 before rebounding to U$ 1.1860 on impressive growth data. Fed held rates steady and characterised economic activity as rising at a “solid rate” firming expectations of a 25 bps rate hike at its December 13 meeting. The new Fed chair Jerome Powell is an existing member of the FOMC and so ensures some continuance of the current policy.

Bank of Japan left monetary policy unchanged, while downgrading its CPI forecasts for fiscal 2017 and 2018. The LDP-led coalition’s election victory also ensures continuity of “Abenomics”. The BoE delivered the 25 bp base rate hike but the dovish spin through their pessimistic growth forecasts, Brexit impact warnings and muted future rate rise expectations caused the pound to plunge toward U$ 1.30. To add to the mess, forty conservative MPs have now signed a no-confidence letter on prime minister’s leadership in May.

Oil prices scaled U$ 65 p/b on global economic recovery, Saudi anti-corruption drive and hopes of extension to Organization of the Petroleum Exporting Countries (Opec) production cuts before International Energy Agency (IEA)’s sober outlook on 2018 oil demand tempered the rally.

The rupee gained to 64.47/U$ as India improved 30 places to 100th place on the World Bank’s ease of business ranking. However, nervousness in emerging market’s asset markets after the oil price rise pushed the rupee back to over 65.50/U$. The 10- year government yields surmounted 7.09% per annum, after September industrial production softened to 3.8%y/y but October CPI rose to 3.58%, a seven-month high on firm vegetable prices. October WPI printed 3.59%, on higher food and fuel prices.

All leading to reduced expectations of a rate cut at Reserve Bank of India (RBI)’s December 6 meeting. October trade deficit widened sharply to a three-year high of U$ 14 billion even as export growth contracted 1% and imports rose 7.6%, slowest in nine months. The surprise export contraction was attributed to festival-related seasonality along with GST related hitches.

Unexpectedly, Moody’s upgraded India’s local and foreign currency rating to Baa2 from Baa3 and changed outlook to stable from positive. It cited continued progress on economic and institutional reforms (Jan Dhan, demonetization, GST and PSU-bank recapitalisation) as enhancing India's high growth potential and its large and stable financing base for government debt and eventually contributing to a gradual, medium-term decline in the debt burden. This news caused the rupee to strengthen dramatically to 64.60 /U$ and government bond yields to gain to 6.935%per annum.

Over the medium-term, we expect rupee to trade the 64.40-65.50 zone.

The writer is president and chief operating officer, Kotak Mahindra Bank